Craft3 cofounders, Mike Dickerson and John Berdes

In Astoria, it’s hard to walk a block without bumping into a Craft3-financed project.

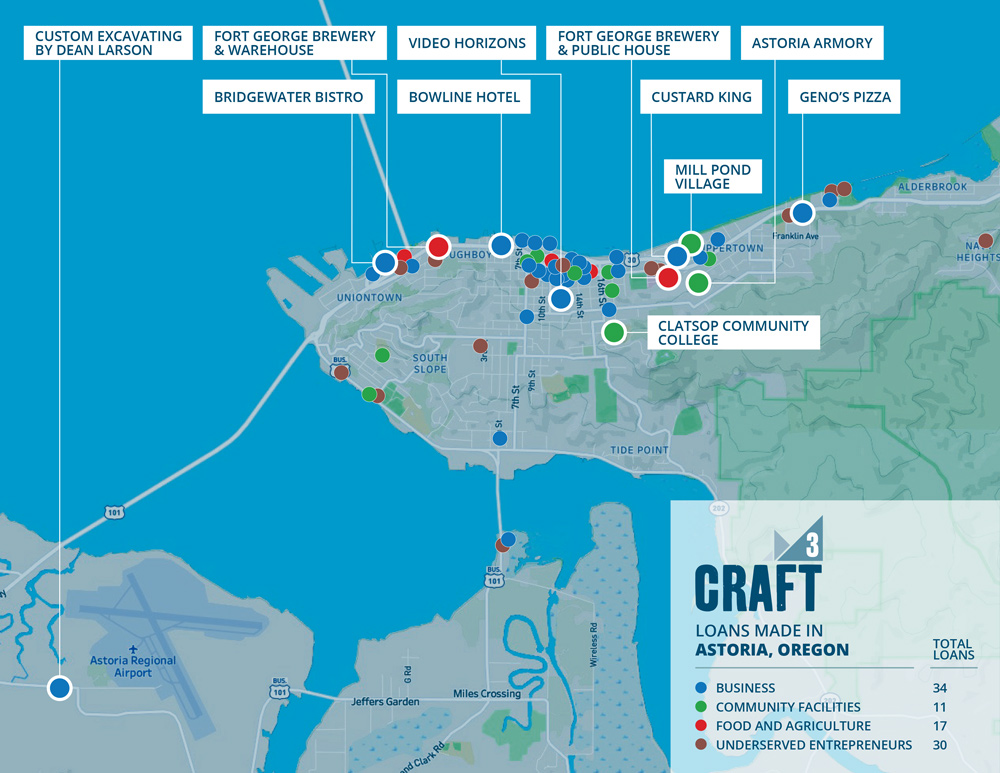

Project by project, and year by year, Craft3 gained experience working in the community of Astoria and delivered significant impacts. Driven by a commitment to finance entrepreneurs unable to get bank financing and guided by a triple-bottom-line approach—focused on social and environmental impacts as well as economic ones—Craft3-financed projects brought good jobs, built housing, and gave Black, Indigenous, or people of color (BIPOC) and women entrepreneurs a chance.

Craft3 has financed more than 90 projects that span Astoria. The Mill Pond Village, Clatsop Community College, and Astoria Armory projects have profoundly changed the city. And two significant, recent Craft3 projects are continuing to transform Astoria’s waterfront and bolster its economy with living-wage jobs and opportunities to build careers.

Tiffany Turner, owner, Bowline Hotel

Bowline Hotel

Chris Nemlowill, cofounder, Fort George Brewery

“We want to be one of the best places you can get a job on the West Coast.”

Chris Nemlowill

Cofounder, Fort George Brewery

Fort George Brewery

Ilwaco, WA